Recent shifts in regulation are widening the doorway for decentralized finance (DeFi) to move from a niche innovation into a core infrastructure layer that could ultimately replace the backend of traditional fintech systems. This trajectory — once speculative — is drawing serious attention from builders, investors, and regulators alike, suggesting that DeFi is evolving into much more than a fringe experiment and may soon underpin large parts of global financial technology operations.

DeFi’s early years were dominated by high-yield experiments and speculative products, but as regulatory clarity has improved, projects with real-world utility have gained momentum. Market participants and builders now see a future where financial services are powered by decentralized protocols rather than traditional rails — potentially transforming the way payments, lending, trading, and liquidity provision are structured.

\Why DeFi Could Become the Financial Backbone

One of the most powerful drivers behind this shift is regulatory progress. Legislation such as the U.S. GENIUS Act of 2025 — which provides clearer guardrails for stablecoins — and growing international discussions about compliant digital asset frameworks have greatly reduced uncertainty. This has encouraged both DeFi builders and some incumbent players to innovate with confidence.

Stablecoins, in particular, are emerging as a fundamental building block of decentralized financial infrastructure. Their ability to offer predictable value transfer without relying on traditional banking rails makes them especially attractive for global payments and settlement. Developers argue that by embedding stablecoins and smart contract-based systems underneath front-end services, companies can achieve faster settlement, lower costs, and more transparent flows compared with legacy systems — all without sacrificing compliance.

Moreover, DeFi-based trading and liquidity protocols are gaining traction. Projects like Hyperliquid are already offering features similar to centralized exchanges — such as low-latency trading and visible order books — while fully embracing decentralized settlement. These developments are reducing the gap between crypto-native tools and mainstream financial services.

Regulatory Clarity and Institutional Involvement

Regulatory clarity has been essential to DeFi’s maturation. The removal of persistent uncertainty — especially around stablecoins and foundational infrastructure — has opened the door for more robust compliance models and institutional engagement. Regulators in certain jurisdictions are now creating frameworks that treat digital cash and blockchain settlement as legitimate and regulated financial infrastructure, rather than sideline experiments.

This regulatory evolution is producing real effects:

- DeFi lending and borrowing platforms now offer features akin to deposit and credit services, often with built-in insurance mechanisms that cover user deposits.

- Trading protocols on decentralized ledgers provide low friction execution and custody alternatives to legacy systems.

- Integration with mainstream partners is tangible, as projects originally seen as niche now collaborate with wallet providers, exchanges, and fintech services on compliant rails.

As traditional finance grapples with its own regulatory pressures — including requirements to fully onboard and understand customer activity — DeFi’s transparent, audit-friendly nature becomes a distinct competitive advantage.

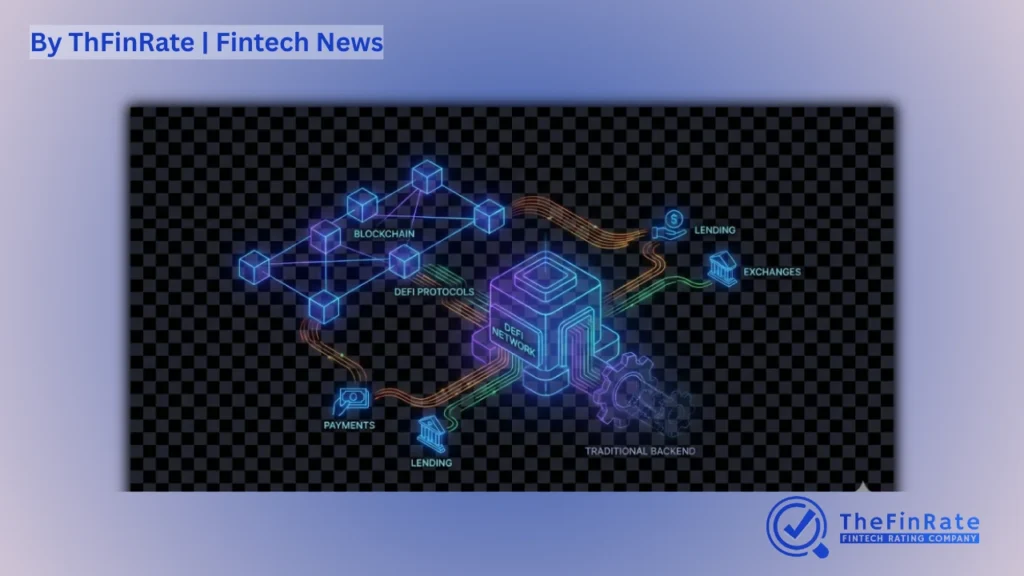

The Fintech Backend of Tomorrow

The idea that DeFi could replace traditional fintech infrastructure does not imply that banks or established finance players will suddenly disappear. Rather, it suggests a reallocation of roles: fintechs may continue to own the customer experience, but the underlying technology that executes settlement, credit, and liquidity functions could increasingly reside on decentralized protocols.

This trend has been described by some developers as the “DeFi mullet” — the frontend remains familiar and user-focused, while the backend transforms into decentralized infrastructure that is faster, cheaper, and more transparent. This hybrid model allows fintech firms to combine regulatory compliance and user experience with DeFi’s operational efficiency.

In practice, this means:

- Payments and settlement may move to stablecoin-based rails with on-chain finality.

- Lending and credit markets might use decentralized liquidity pools instead of traditional interbank networks.

- Trading and asset transfer could increasingly occur through smart contract-based protocols with open settlement data.

For end users and businesses, these changes could translate into faster processing times, lower fees, and greater transparency — without sacrificing the trust and compliance needed to operate at scale.

Challenges and the Road Ahead

Despite this momentum, several challenges remain before DeFi can universally replace traditional backends. Regulatory alignment is still uneven across jurisdictions, and smart contract security, risk management, and institutional adoption barriers persist.

Security concerns — including hacks, smart contract vulnerabilities, and systemic risk — require robust frameworks and risk controls before decentralized infrastructure can universally replace legacy systems.

Moreover, while regulatory clarity is improving in some regions, global regulatory divergence continues to complicate cross-border integration and coordination. In the absence of harmonized standards, fintechs and institutions must navigate complex compliance landscapes and avoid potential arbitrage risks.

Still, the direction of travel is evident. As regulators focus on enabling innovation while managing risk, DeFi’s role in the financial ecosystem continues to expand. The technology is no longer just a speculative corner of crypto markets — it is evolving into a compliance-aware backbone that could redefine the infrastructure underpinning future financial services.

Conclusion

As regulatory barriers fall and DeFi ecosystems mature, the boundary between decentralized and traditional finance is thinning. With stablecoins, smart contracts, and compliant protocols gaining traction, DeFi offers a compelling alternative to legacy backend systems — one that prioritizes speed, transparency, and efficiency.

While full replacement of traditional infrastructure is a long-term outcome contingent on regulatory alignment and technological evolution, the shift toward decentralized backend systems is already underway. For fintechs, institutions, and investors, this represents a strategic inflection point in how financial services are built and delivered in the coming decade.